Right now, someone in Mumbai is watching a cricket match on JioHotstar while their teenager plays a mobile RPG with friends in Seoul and São Paulo. In Los Angeles, a mid-size brand is running shoppable video ads on a connected TV. In Lagos, a creator with 2 million TikTok followers just monetized a clip that cost nothing to produce. And in a server farm outside Amsterdam, an AI model is generating subtitles in 47 languages for a drama no human translator has touched.

This is what the media and entertainment industry looks like in 2026. It is not one industry anymore. It is a sprawling, fast-moving ecosystem of screens, platforms, algorithms, creators, advertisers, and experiences — and it is enormous. The global M&E market generated $3.5 trillion in total revenues in 2025, and it is growing. For marketers, investors, content builders, and C-suite decision-makers, the statistics that define this space are not just interesting numbers. They are the map you navigate by. This article gives you that map, fully updated through 2026 with projections to 2030.

Editor’s Snapshot: Key Numbers at a Glance

These are the most strategically important figures in the industry right now, each with a brief note on why it matters.

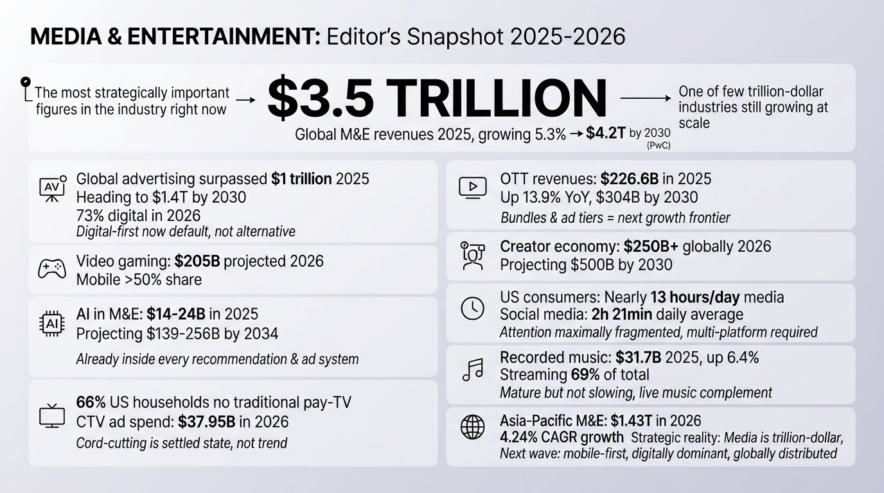

Global M&E revenues hit $3.5 trillion in 2025, growing 5.3%, and are forecast to reach $ 4.2 triliun oleh 2030 at a 3.4% CAGR (PwC). This makes M&E one of the few trillion-dollar industries still growing at scale.

Global advertising surpassed $1 trillion in 2025 for the first time, menuju ke arah $ 1.4 triliun oleh 2030, with digital claiming 73% of total global ad spend in 2026. Signals that digital-first ad strategies are now the default, not the alternative.

Total OTT revenues reached $226.6 billion in 2025, rising 13.9% year-over-year, projected to reach $ 304 miliar 2030. Bundle strategies and ad-supported tiers are the next growth frontier for streaming platforms.

Video gaming revenue is projected at $205 billion in 2026, with mobile gaming holding over 50% of total share. Gaming is now central to culture, not peripheral to it — a must-have channel for brand experiences.

The creator economy is valued at over $250 billion secara global pada tahun 2026, with analysts projecting $ 500 miliar 2030. Creators are not supplemental to media strategy; they are an independent distribution layer.

AI in media and entertainment was valued at $14–24 billion in 2025, with projections ranging to $139–256 miliar pada tahun 2034 depending on the research source. AI is not coming to media. It is already inside every recommendation engine, ad targeting system, and production workflow.

US consumers are projected to spend nearly 13 hours per day across media, with average global social media use at 2 hours 21 minutes daily. Attention is maximally fragmented. Reach now requires multi-platform presence, not single-channel dominance.

66% of US households no longer subscribe to traditional pay-TV, Sementara CTV ad spend hits $37.95 billion in 2026. Cord-cutting is not a trend. It is the settled state of American media consumption.

Global recorded music revenue grew 6.4% to $31.7 billion in 2025, with streaming accounting for 69% of that total. Music streaming is mature but not slowing, and live music is its fastest-growing complement.

The Asia-Pacific M&E market is worth $1.43 trillion in 2026, tumbuh pada CAGR 4.24%. APAC is where the next wave of growth happens — mobile-first, multilingual, and driven by local content.

Global Market Size and Growth (2025–2030)

Overall Market Size and CAGR

The global entertainment and media industry generated $ 3.5 triliun dalam 2025, according to PwC’s Global Entertainment and Media Outlook 2026–2030, covering 12 segments across 53 territories. The industry grew at 5.3% in 2025 and is forecast to grow a further 4.6% in 2026. Over the full five-year horizon to 2030, PwC projects a 3.4% CAGR, tiba di $ 4.2 triliun in total annual revenue. That means approximately $600 billion in new revenue will be unlocked between now and 2030 — an extraordinary figure that helps explain why capital continues to flood into the sector despite the much-discussed profitability struggles of individual players.

The three main revenue pillars are connectivity (the largest, at approximately $1.3 trillion annually), advertising (the fastest growing), and consumer content spending (the most structurally disrupted). Connectivity will grow modestly at a 2.3% CAGR to $1.5 trillion by 2030 as broadband becomes commoditized. Internet advertising, on the other hand, accelerated by 12.2% in 2025 alone to reach $ 755.6 miliar dan diperkirakan akan menghantam $ 1.1 triliun oleh 2030 — the single most dynamic revenue pool in the industry.

The Structural Shift from Traditional to Digital Revenue

Traditional television revenues fell 2.7% in 2025 to $360.5 billion and will continue declining at a 0–1.1% CAGR through 2030, ending at approximately $341 billion. Meanwhile, digital formats including OTT video, internet advertising, digital music, digital publishing, and digital OOH are collectively gaining share every year. By 2030, digital will account for an overwhelming majority of industry revenue. The strategic implication is not subtle: any media business still primarily organized around linear, traditional formats is managing decline, not building for growth.

Distribusi Wilayah

Daerah | 2026 Market Size (est.) | Penggerak Pertumbuhan |

Amerika Utara | Pasar tunggal terbesar | Subscription saturation pushing ad-supported tier growth |

Asia Pacific | $1.43 trillion (CAGR 4.24%) | Mobile-first audiences, local language content, cricket and K-drama |

India | ~$30.9 billion (2026 est.), growing ~5.8% CAGR to 2028 | JioHotstar, vernacular OTT, 4th largest TV ad market by 2026 |

Eropa | Mature with consolidation activity | Public broadcaster partnerships with streaming giants |

Pasar negara berkembang | High percentage growth rates | Internet penetration, mobile payment, and creator economy expansion |

North America remains the biggest single revenue pool, but it is also the most saturated market for subscriptions. Asia-Pacific is where growth rates are structurally higher, driven by a population that skipped desktop internet and went straight to mobile, combined with intense local content competition. India deserves specific mention: it is becoming a battleground for OTT platforms, with premium AVOD revenues expanding rapidly and CTV usage accelerating post-2026. Latin America’s eCommerce and creator economy sectors are each growing over 20% annually.

For businesses making expansion decisions, the data points toward regional content localization as a non-optional investment, not a nice-to-have.

Segment Breakdown: Where the Revenue Actually Lives

Ruas | Revenue (2025–2026) | Tren Pertumbuhan | Primary Monetization |

TV tradisional | $360.5B (2025, falling) | Declining (−2.7%) | Ad sales, carriage fees |

OTT / Streaming Video | $226.6B (2025 OTT total) | High growth (13.9% in 2025) | Subscriptions + ads |

Film / Box Office | Recovering; $39.5B by 2030 | Moderate (CAGR 3.2%) | Ticket sales, premium formats |

Music (total market) | $ 125.9 miliar (2025) | Steady (to $145.8B by 2030) | Streaming subs, live events, licensing |

Video Games & Esports | $205B+ (2026 proj.) | High growth (4.6%+ YoY) | Microtransactions, subs, ads |

Taruhan Online | $79.5B GGR (2025) | Very high (CAGR 8.5% to 2030) | Stakes, house margin |

Publishing (digital) | Moderat | Flat to moderate | Subscriptions, licensing |

Di Luar Rumah (OOH) | $37.9B rising to $45.8B (2030) | Moderate (CAGR 3.9%) | Ad placements, digital inventory |

Gaming deserves a sharp strategic note here. With over $ 205 miliar in projected 2026 revenue and a player base that now represents nearly half the world’s population, video games are not a niche media product. The combination of deep daily engagement, in-game spending behavior, and immersive brand placement opportunities makes gaming the most compelling new advertising frontier in the industry. When a cosmetics brand launches a limited skin in Fortnite, it generates more user attention per dollar than almost any traditional format can match.

The return of cinema is also worth noting. Box office revenue is recovering with a CAGR of 3.2%, heading toward $39.5 billion by 2030. The driver is not nostalgia: it is the growing value of shared, immersive, non-replicable experiences. Luxury seating, large-format screens, and the social currency of attending a cultural event are drawing audiences back, particularly for event films. The same logic applies to the explosive growth of live music (heading above $41.5 billion by 2030) and the emergence of destination entertainment venues like Sphere in Las Vegas, which alone generated $781 million in 2025 revenue.

Streaming & OTT: Subscriptions, Cord-Cutting, and What Comes Next

The Scale of Streaming and the Onset of Fatigue

Total global OTT revenues reached $ 226.6 miliar 2025, a 13.9% increase from 2024’s $199 billion. Projections place this at $ 304 miliar 2030, but the growth rate will slow as markets mature. In Australia, Spain, South Korea, and North America, subscription fatigue is becoming measurable. The concept of consumers paying for multiple streaming subscriptions simultaneously is hitting a natural ceiling.

Di Amerika, 66% of households no longer subscribe to traditional pay-TV as of early 2026, with cable subscribers falling from 105 million in 2010 to approximately 68.7 million in 2026. The cord has been cut. What consumers are doing instead is subscribing to streaming services — but increasingly, they are managing costs by rotating, pausing, or substituting subscriptions rather than stacking them indefinitely.

The Rise of Ad-Supported Streaming

The industry’s structural response to subscription saturation is the aggressive development of ad-supported tiers. OTT advertising, currently 19.4% of OTT revenues, will grow at a 9.4% CAGR untuk mencapai 22.6% of OTT revenues by 2030. Netflix’s advertising revenue more than doubled in 2025 to over $1.5 billion. Amazon Prime Video defaulted its entire subscriber base to an advertising tier in 2025, reaching 315 million monthly ad-supported viewers globally — larger than Netflix’s ad-reach. Disney+, Paramount+, and Peacock are all expanding their advertising technology stacks. The ad-supported streaming tier is no longer a discount product. It is becoming the dominant consumption model.

Device Use and CTV

Connected TV advertising spend will reach $ 37.95 miliar 2026, with CTV surpassing linear TV in daily viewing time for the first time. 57% of viewers say they prefer CTV ads over traditional linear TV ads, dan 70% of advertisers plan to increase CTV spending by approximately 17%. YouTube, meanwhile, now holds 12.5% of all US TV viewing time (the highest of any single streaming service per Nielsen), with TV screens having officially overtaken mobile as the primary YouTube viewing device in the US.

This points toward a fundamental reorientation: the living room screen is becoming a digital screen, and the advertising technology, targeting capability, and measurement frameworks of digital media are becoming the standard for television advertising.

Social Media, Short-Video, and the Creator Economy

Platform Scale and Time Spent

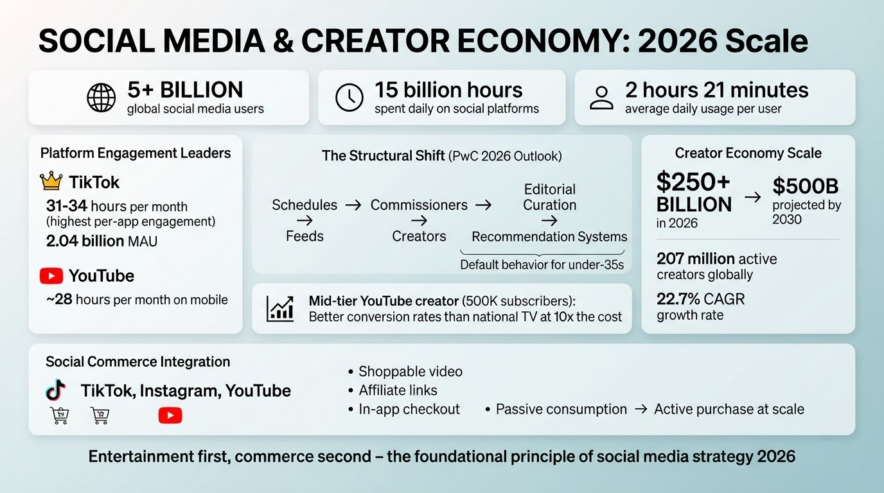

Sekarang ada lebih dari 5 miliar pengguna media sosial global, collectively spending approximately 15 billion hours per day on social platforms. The average user spends 2 hours 21 minutes daily on social media, but TikTok users average 31–34 hours per month on the app alone — the highest per-app engagement figure of any major platform. YouTube comes second with approximately 28 hours per month on mobile.

TikTok’s global monthly active user base has reached 2.04 miliar, Instagram and Facebook maintain multi-billion user bases, and regional platforms — Douyin and Kuaishou in China, ShareChat and Moj in India — are carving significant audiences in markets the Western platforms do not fully reach.

The Creator Economy at Scale

The global creator economy is estimated at lebih dari $250 miliar pada tahun 2026, with projections toward $ 500 miliar 2030. Ada lebih 207 million active creators globally, and the market is growing at approximately a 22.7% CAGR. What was once dismissed as a side hustle ecosystem now rivals traditional media distribution in both audience reach and advertiser interest. A mid-tier YouTube creator with 500,000 engaged subscribers often delivers better conversion rates for product categories than a national television placement at ten times the cost.

PwC’s 2026 Outlook describes a structural shift in content discovery: “audiences will increasingly discover content through feeds rather than schedules, creators rather than commissioners, and recommendation systems rather than editorial curation.” This is not a forecast. It is already the default behavior for anyone under 35.

Social Commerce and Purchase Influence

Social platforms are increasingly shortening the distance between content discovery and purchase. For brands, designing content that operates as entertainment first and commerce second is now the foundational principle of social media strategy. The integration of shoppable video, affiliate links, and in-app checkout features across TikTok, Instagram, and YouTube is turning passive content consumption into active purchase behavior at scale.

Gaming, Esports, and Interactive Media

Video games are projected to generate $ 205 miliar 2026 — more than the global box office and music industries combined. Mobile gaming accounts for over 50% of total gaming revenue, making smartphone gaming the largest single platform segment in entertainment. Console and PC gaming remain high-value, high-engagement segments, particularly for premium narrative games and live-service titles that generate recurring microtransaction revenue.

The crossovers between gaming and other media are multiplying rapidly. Musicians hold in-game concerts with tens of millions of attendees. Film franchises launch as simultaneous cinematic and gaming experiences. The NFL, NBA, and Premier League all have dedicated esports and gaming strategies. Esports audiences and revenue continue to grow, particularly in Asia-Pacific markets, with in-game advertising and branded experiences emerging as a category that deserves dedicated investment from any brand seeking to reach young male audiences specifically.

Looking forward, cloud gaming’s potential to remove hardware barriers from high-quality gaming experiences could significantly expand the addressable market, particularly in emerging economies where console ownership remains low.

Advertising, Brand Spend, and Programmatic

Global ad spend hit a record $ 1.3 triliun dalam 2026, a 9.1% increase from 2025 according to WARC. Digital advertising commands 73% of total global media spend, with the global digital advertising market valued at $ 662.3 miliar 2026 dan diproyeksikan untuk dicapai $ 1.69 triliun oleh 2033. Internet advertising alone accelerated 12.2% in 2025 to $755.6 billion and is heading toward $1.1 trillion by 2030.

Several format shifts are reshaping where budgets actually flow:

Media ritel is capturing an increasing share of search budgets. Amazon’s advertising revenue reached $68 billion in 2025. Walmart’s retail media revenue topped $6.4 billion. These are shopping-intent audiences at the point of purchase — the most commercially direct targeting possible.

Iklan TV yang terhubung is at $37.95 billion in 2026 and growing as streaming platforms build out their ad tech infrastructure.

Programmatic digital OOH is growing at a 9.2% CAGR, reaching $26.5 billion by 2030 as outdoor advertising becomes dynamic, data-driven, and real-time.

Perdagangan sosial is compressing the funnel from discovery to transaction within a single platform session.

Conversational search via AI (ChatGPT, Gemini) represents a structural threat to traditional paid search, pushing brands to think about generative engine optimization (GEO) alongside SEO.

For media planners, the core challenge of 2026 is fragmentation: audiences are distributed across more surfaces than any single plan can fully cover, and measurement consistency across those surfaces remains genuinely difficult. First-party data strategy, clean room partnerships, and platform-native measurement tools are the infrastructure investments that determine whether attribution is accurate enough to optimize.

AI, Automation, and Emerging Tech in Media

AI in media and entertainment was valued at between $14 billion and $28 billion in 2025–2026 depending on the research methodology, and multiple forecasts project this figure reaching $139–256 miliar pada tahun 2034. The range reflects the definitional challenge of measuring AI that is embedded inside larger platforms rather than sold as a standalone product.

In practical terms, AI is already embedded in every major dimension of the M&E value chain: recommendation engines (Netflix, Spotify, YouTube), ad targeting (Google, Meta, Amazon), content translation and dubbing for global distribution, AI-assisted editing and production tools, personalized newsletter generation, and increasingly, synthetic media creation. The OmnicomIPG merger in 2025 explicitly cited AI-driven campaign optimization as central to its rationale. Publicis paid $2.2 billion for LiveRamp in mid-2026 specifically to strengthen its data, identity, and AI-enabled media buying capabilities.

The strategic opportunity for smaller creators and regional media companies is particularly significant. AI tools are dramatically lowering the cost and technical barrier for high-quality production, multilingual distribution, and algorithmic content optimization — capabilities that previously required either scale or substantial budgets. A regional-language content creator in Tamil Nadu or a digital-native publisher in Eastern Europe can now compete for audience attention at a quality level that was impossible five years ago.

The risks are equally real. Consumer trust in AI-generated content is conditional: audiences accept AI-assisted production and personalization but show measurable skepticism toward fully synthetic journalism, deepfake entertainment, and AI-authored creative work. Brands and platforms that use AI in ways that feel deceptive — rather than efficient or personalized — face genuine reputational exposure as literacy about AI grows among general audiences.

Consumer Behavior: Attention, Devices, and Churn

US consumers are projected to engage with media across nearly 13 hours per day in 2026, a figure that sounds implausible until you account for simultaneous device usage: someone watching television while scrolling Instagram and listening to a podcast has technically consumed three media simultaneously. Multi-screen behavior is now the norm rather than the exception, and second-screen usage during television viewing is a mainstream behavior that fundamentally changes how advertising during a broadcast can function.

Device split data reinforces the mobile-first reality covered earlier, with smartphones leading total time spent, connected TVs gaining share for premium long-form content, and laptops and desktops remaining important for work-adjacent media consumption. Smart speakers are growing as a distribution channel for audio content, particularly podcasts and music, with podcast monthly listeners reaching new highs in multiple markets.

Subscription churn is a defining business challenge for streaming platforms. The primary driver is simple: cost pressure. As subscription counts per household have grown and prices have risen, consumers are more willing to cancel a service after a binge-watch and resubscribe later. Platforms are responding with bundle offers, annual billing discounts, and feature additions — but the longer-term fix may be the shift to ad-supported models that are cheaper to enter and less likely to trigger active cancellation.

Jobs, Skills, and the Workforce Transformation

The US media and entertainment workforce is facing its most significant structural change since the shift from print to digital. AI is not replacing creativity, but it is rapidly automating many of the production, distribution, and analytical tasks that mid-level roles previously performed. PwC’s 2026 AI Jobs Barometer found that AI is creating a two-track labor market: workers who can combine creative or strategic expertise with AI fluency are commanding significant wage premiums, while roles that involve purely routine media processing tasks face automation pressure.

The most in-demand skills across the industry in 2026 are data analytics, AI prompt engineering and workflow design, community management at scale, multilingual content strategy, ad tech and measurement expertise, and the ability to produce high-quality short-form video independently. The talent gap is real and documented: digital transformation projects across media companies consistently cite the inability to hire people who combine both creative and technical fluency as their primary bottleneck — not budget, not technology.

For organizations, this makes continuous upskilling investment not a HR expense but a competitive capability. For individual professionals, the window to develop AI literacy alongside domain expertise is wide open and closing.

Sustainability and Responsible Media

The environmental footprint of the media industry is increasingly scrutinized by audiences, investors, and regulators. Streaming infrastructure is a significant and growing consumer of electricity: data centers serving global video delivery account for a substantial and rising share of digital’s overall energy use. The streaming industry has begun addressing this through investments in renewable energy for server infrastructure, codec efficiency improvements that reduce bandwidth consumption per stream, and sustainability reporting standards borrowed from adjacent tech sectors.

On the production side, the film and television industry’s green production movement has gained meaningful momentum since the pandemic-era reassessment of workflow assumptions. Productions certified under green frameworks are standard for major studio releases in North America and Europe, and ESG reporting requirements are beginning to touch media companies’ operations in ways that will make sustainability performance a competitive and financial consideration, not just a reputational one.

Consumer expectations are also shaping this: younger audiences, particularly Gen Z, show consistent preference for brands and platforms that demonstrate genuine environmental commitment over those that perform it cosmetically.

Pelajaran Praktis bagi Berbagai Pemangku Kepentingan

For Marketers and Advertisers

The digital share of ad spend at 73% globally means legacy channel loyalty is now actively costly. CTV and retail media deserve dedicated line items in any 2026 plan, not experimental allocations. First-party data infrastructure is not optional: as AI-powered targeting becomes standard, the quality of your audience data determines the ceiling of your campaign performance. Creator partnerships in your target demographic will consistently outperform equivalent buys in traditional placements for consideration and conversion metrics. And the shift to generative engine optimization means your brand presence in AI search results needs active management, not passive hope.

For Media Companies and Platforms

The bundle is back, but in a different form. Single-product subscriptions face structural churn pressure; platforms that can offer entertainment, sports, gaming, and social content in one interface will reduce cancellation intent significantly. Content localization is a revenue unlock, not a cost: India, Southeast Asia, and Latin America offer the highest growth rates for OTT platforms willing to invest in regional language content. Ad-supported tiers should be treated as a primary product, not a fallback. And the acquisition of premium IP — sports rights, franchise content, live events — is the most defensible asset in a platform economy.

For Creators and Influencers

The creator economy at $250 billion is real, but it is also consolidating. The mid-tier creator with deep niche engagement is more commercially viable than the mega-influencer with broad but shallow reach in many product categories. AI tools for production, translation, and SEO optimization are now accessible at low cost — using them is a capability multiplier, not cheating. Diversification across revenue streams (brand deals, subscriptions, digital products, live events) is risk management: no platform’s algorithm is stable enough to be your only income source. And cross-platform distribution — building audience on TikTok, monetizing on YouTube, selling through Substack or Patreon — is the professional creator’s standard operating model in 2026.

For Investors and Policymakers

The $600 billion in projected new M&E revenues by 2030 is not evenly distributed: it flows toward platforms with AI infrastructure, first-party data advantages, live content rights, and emerging market presence. Consolidation will continue: the Paramount-Warner Bros. Discovery deal, the Comcast-ITV deal, and the Omnicom-IPG agency merger are harbingers of further M&A as legacy profit pools shrink and scale becomes the primary competitive differentiator. For policymakers, the dominance of US-headquartered platforms in global digital advertising and the competitive pressure on public service broadcasters represent regulatory questions that are moving from theoretical to urgent in markets across Europe, India, and the Asia-Pacific.

Conclusion: What 2027–2030 Will Actually Look Like

The data in this article points toward a 2030 media and entertainment landscape that is more AI-augmented, more live and experiential, more creator-distributed, and more regionally diverse than anything that came before it. The platforms that dominate will be those that can simultaneously offer the scale and efficiency of algorithmic systems with the authenticity and creative originality that only human craft produces. AI will not replace that craft. It will amplify it — and create an increasingly steep separation between those who use it strategically and those who do not.

Four forces will define the next four years above all others: Personalisasi (the expectation that every content and advertising experience is relevant to you specifically), percaya (the premium that audiences place on authentic, transparent, non-synthetic media in a world flooded with AI-generated content), keberlanjutan (the growing regulatory and consumer pressure on both content and infrastructure to reduce environmental impact), and pengalaman lintas platform (the recognition that no single screen, platform, or format owns the consumer’s attention journey from discovery to purchase to loyalty).

Media and entertainment is not just an industry. It is the infrastructure through which culture is transmitted, commerce is transacted, and attention — the scarcest resource of the modern economy — is earned and held. The businesses that treat it that way, and let data lead their decisions within it, are the ones that will own the next chapter.

Pertanyaan yang Sering Diajukan

The global media and entertainment industry is projected to surpass $3 trillion by 2030, driven by rapid digital adoption, streaming growth, and expanding emerging markets. Compound annual growth rates are expected to average between 7% and 10% through the forecast period.

Streaming services will continue to dominate content consumption, with subscriber bases expanding significantly across Asia-Pacific, Latin America, and Africa. Competition among platforms will intensify, pushing investment in original content and AI-driven personalization to new highs.

Yes, the gaming sector is one of the fastest-growing segments and is expected to outpace several traditional entertainment categories, including linear TV and physical media. Cloud gaming and mobile gaming are key drivers fueling this accelerated growth trajectory.

Asia-Pacific benefits from a massive and rapidly expanding middle class, increasing smartphone penetration, and government investments in digital infrastructure. Countries like India, China, and Indonesia are expected to contribute disproportionately to global revenue growth between 2026 and 2030.

Absolutely, AI is transforming content creation, ad targeting, audience analytics, and content moderation, creating new revenue streams and reducing operational costs. Industry analysts forecast that AI-driven solutions could contribute hundreds of billions of dollars in added value to the sector by 2030.